In order to capitalize on the financial structuring expertise of Falvez Energy L.L.C. (Falvez Energy) principals and the local expertise of energy developers (Local Partners), a strategy was devised that each project will have significant inputs from Local Partners in the structuring of the projects (i.e., licenses, land agreements, Power Purchase Agreements (PPA), interconnection agreements), the commissioning of the projects (i.e., Equipment Procurement Construction (EPC) contracts), and in the operations of the projects (i.e., Operation and Maintenance Agreement (O&M)).

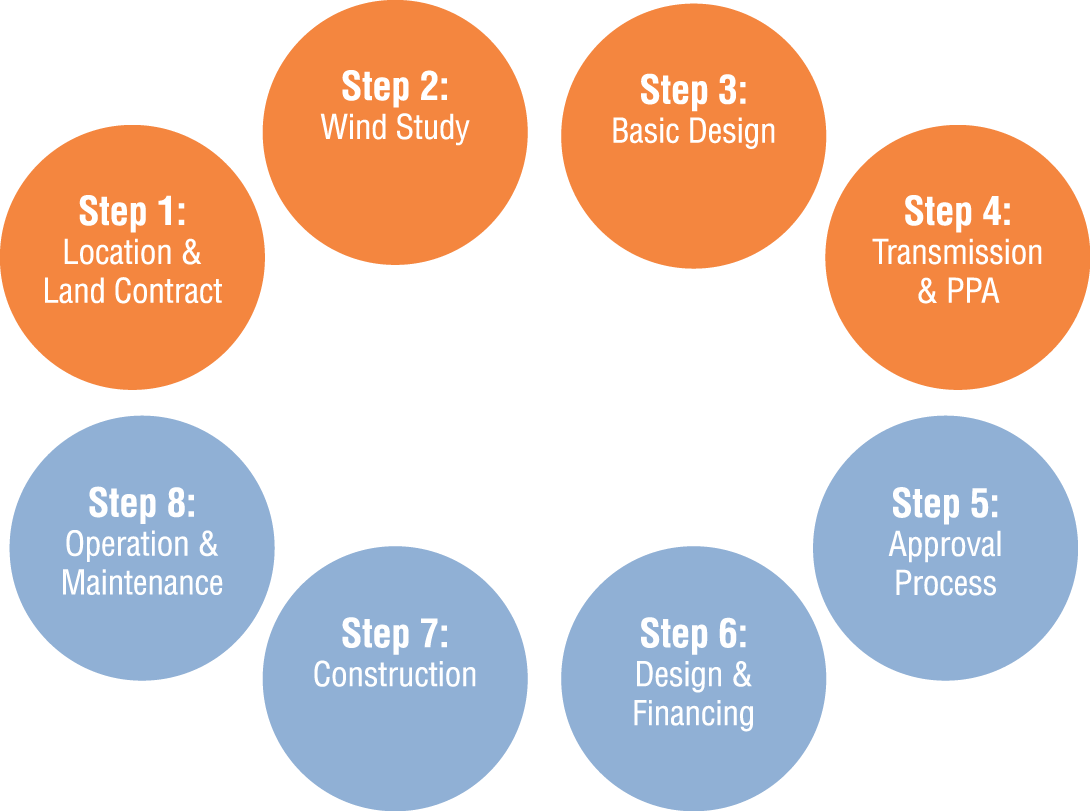

Each project can be broken down into four phases with a number of steps (see Steps in Figure 1) in each phase: (i) Initial Development (Steps 1, and Step 2); (ii) Final Development, Equity and Debt Due Diligence, and Financial Closing (Steps 3, 4, 5, and 6); (iii) Commissioning of EPC (Step 7); and (iv) Project Completion and Operation and Maintenance (Step 8).

In order to expedite the project development cycle and to make certain that Financial Closing (i.e., the last occurrence in Step 6 below), occurs as soon as possible, the initial two phases will have most of the necessary attributes required by both Falvez Limited Partners for equity (Falvez LP) as well and senior debt financiers (Senior Lenders) to participate.

The strategy behind Falvez Energy is to mitigate most of the risks for both Falvez LP, as well as the Senior Lenders. As such, Falvez Energy will utilize its own resources to get the projects to Financial Closing, where at Financial Closing both equity (from Falvez LP), and debt (from Senior Lenders) would enter pari-pasu in the project, mitigating for Falvez LP two important structuring challenges: (i) funding gap; and (ii) contingent equity obligations (i.e., in order to mitigate contingent equity obligations, full wrap EPC is expected)[1]. In addition Falvez Energy projects are expected to have the following characteristics: (i) projects is economically competitive with-out government subsidies (i.e., feed-in tariffs); (ii) is sized to off-set the development costs (i.e., approximately of 100-Megawatt (MW) or two or more 30-MW under the Costo Total de Corto Plazo (CTCP)); (iii) land projects are located in private land, or communal land that has been partitioned; (iv) wind resources have been micro-sighted (i.e., Measuring Towers have been installed, certified and monitored; and or spatial sighting have been verified); (v) off-takers are private and credit worthy or CFE under the CTCP Mechanism; and (vi) long-term land lease or land purchase agreements are in-place, with the possibility of renewal.

Life of a Wind Project

Location & Land Contract

Identification of promising location

Land Contract (Ownership or Leasing)

Preliminary collection of wind

Wind Study

Selection of equipment manufacturer;

Equity due diligence (wind, land, env.)

Feasibility study (full equity secured)

Basic Design

Wind assessment & generating capacity (18 months)

Initial study of economic viability

Transmission & PPA

Consultation with CFE about connection to transmission lines

Power Purchase Agreement (PPA)

Approval Process

Environmental Impact Assessment (EIA)

Building Codes and Ordinance

Construction

Civil engineering work

Electrical construction work

Test operation and inspection

Design & Financing

Debt financing due diligence

Financing (full debt financing secured)

Financial closing

Operation & Maintenance

Supervision of operation conditions

Facility maintenance

Identification of promising location

Land Contract (Ownership or Leasing)

Preliminary collection of wind

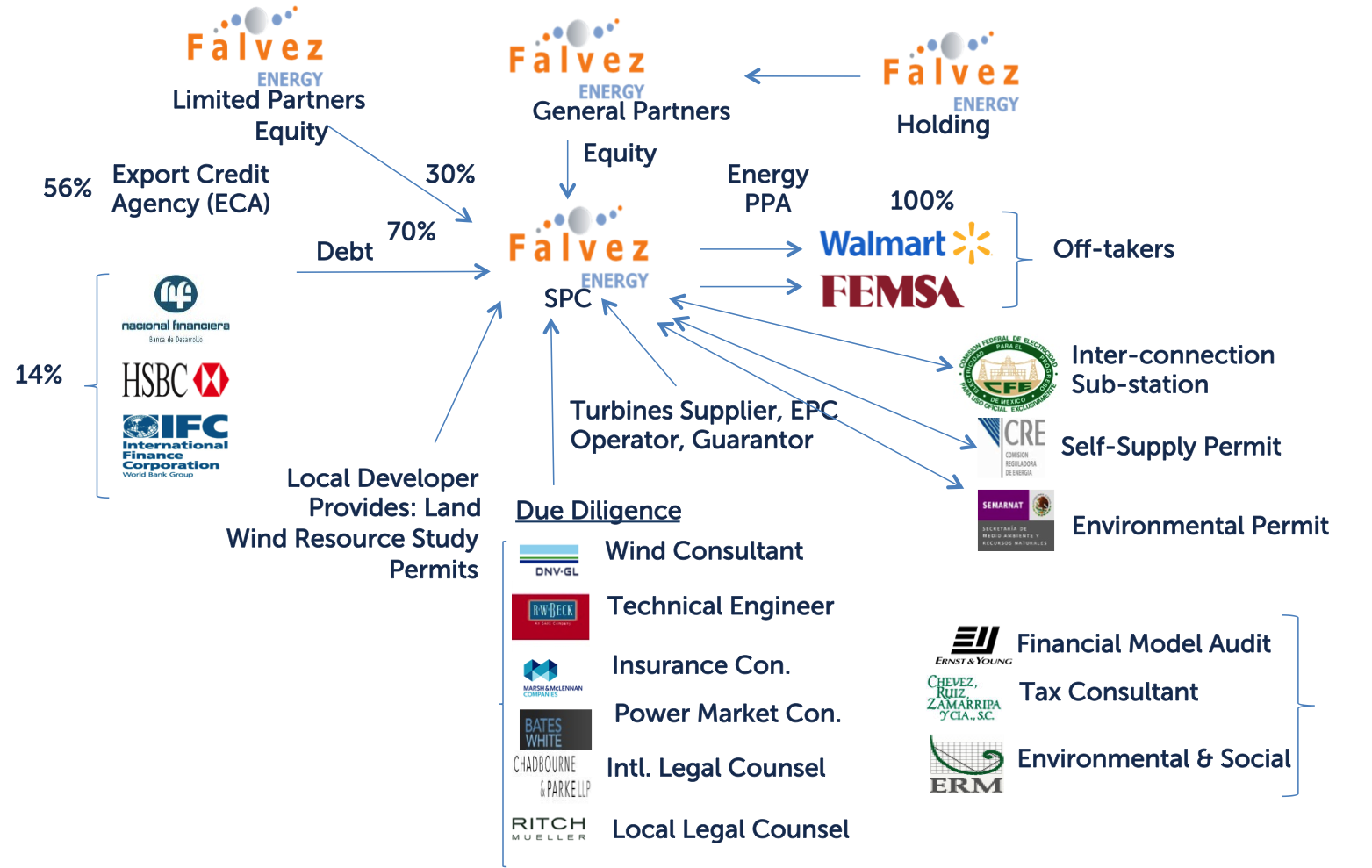

Details on Equity Participation

The division of equity amongst the relevant stakeholders (i.e., Falvez Energy, Local Partners, and Falvez LP) is also innovative in the renewable energy realm. Given that, in the past, the Local Partners may lack financial resources and/or international debt financing expertise, have often develop the projects up to the first two steps (See Figure 1), and an international wind developer acquired the project leaving a relatively small equity percentage to the Local Partners. Falvez Energy, given our business model to form strategic alliances with Local Partners, we have devised a modality in which in the long-run (i.e., summing up the economic useful life of the project, which is typically 15 years to 20 years), the Local Partners obtain a greater financial benefit from such strategic alliance versus selling the initial development to international wind developers.

The Project Company or Special Purpose Company (SPC), which will be registered in the location of the project, would be owned by Falvez General Partners (Falvez GP) and Falvez Limited Partners (Falvez LP) (see Figure 2 below). Falvez GP would be responsible for securing the equity from Falvez LP, the debt from the Senior Lenders, negotiating all of the relevant pending contracts[1], and providing the necessary resources to conclude both the equity and debt due diligence, which would include the hiring of a number of consultancies[2].

Various investors under Falvez LP would be preferred shareholders and would provide the majority of the equity for the project, for illustrative purposes, assume a 100-MegaWatt (MW) wind project that costs US$200 million. Under a 70/30 debt equity split, Falvez LP would provide US$60 million, while the Senior Lenders would provide US$140 million for the project. In the long-run, returns for both Falvez LP and Falvez GP would be the following: (i) given that Falvez LP have preferred shares, Falvez LP would receive the majority of the profits from the project until the project reached a Hurdle Rate[3]. Upon achieving the Hurdle Rate, a different dividend payout split would be established, in which a significant amount of the profit from the project (via dividends) would go towards Falvez GP.

Sample of Falvez Energy Structure for Mexico Wind Projects

Local Developers partnering with Falvez Energy may obtain the following: (i) a payout of current and past third party obligations incurred by the Local Developers in bringing the project to its current form; (ii) at advanced stage development, a monthly pay-out to Local Developers prior to Financial Close for services provided under the project; (iii) a pay-out to the Local Developers at Financial Closing (i.e., part of the development fee); and (iii) an equity carry in Falvez GP, which is expected to be significantly greater than the traditional international wind energy developers are prepared to offer.

Details on Debt Participation

A significant portion of the debt participation is expected to be sourced from the wind turbine manufacture Export Credit Agency (ECA), as such; turbine purchase agreements would be subject to ECA financing. This approach aligns both entities (i.e., Falvez Energy GP, and the turbine manufacture) in securing a substantial portion of the debt financing.

Risks & Mitigants

Risks

Completion Risks

Mitigants – Turnkey EPC Contract

Operating Risks

Mitigants - O&M Agreement

Revenue Risks

PPA Price Risk

Mitigants - Fixed Price PPA

Wind Volume Risk

Turbine Unavailability

Mitigants - O&M Agreement including Availability Guarnatee

Low Wind

Mitigants - P90 modeling for debt sizing 1.3 DSCR P99 modeling for debt sizing 1.0 DSCR

Electricity Grid Defualt

Mitigants - CFE Interconnection Agreement

Latest Headlines

Wind Power Rivals Coal with $1 Billion Order From Buffett

The decision by Warren Buffett’s utility company to order about $1 billion of wind turbines for projects in Iowa shows how a drop in equipment costs is making renewable energy more competitive with power from fossil fuels. Turbine prices have fallen 26 percent worldwide since the first half of 2009…‘If Congress were to remove all the subsidies from every energy source, the wind industry can compete on its own,’ Kiernan said at a press conference at a Siemens factory in Fort Madison, Iowa, yesterday, when the order was announced.

Bloomberg Sustainability

Wind Muscles Out Other Renewables

Wind farms were the sole winners in Brazil’s 18 November new energy auction, which the government contracted 39 projects with a combined capacity of 867.6-MW. The average price for the energy sold in the auction was US¢5.45/KWh…Projects should be ready to supply the grid by January 2016. Total investment of BR$3.3 billion (US$1.4 billion)